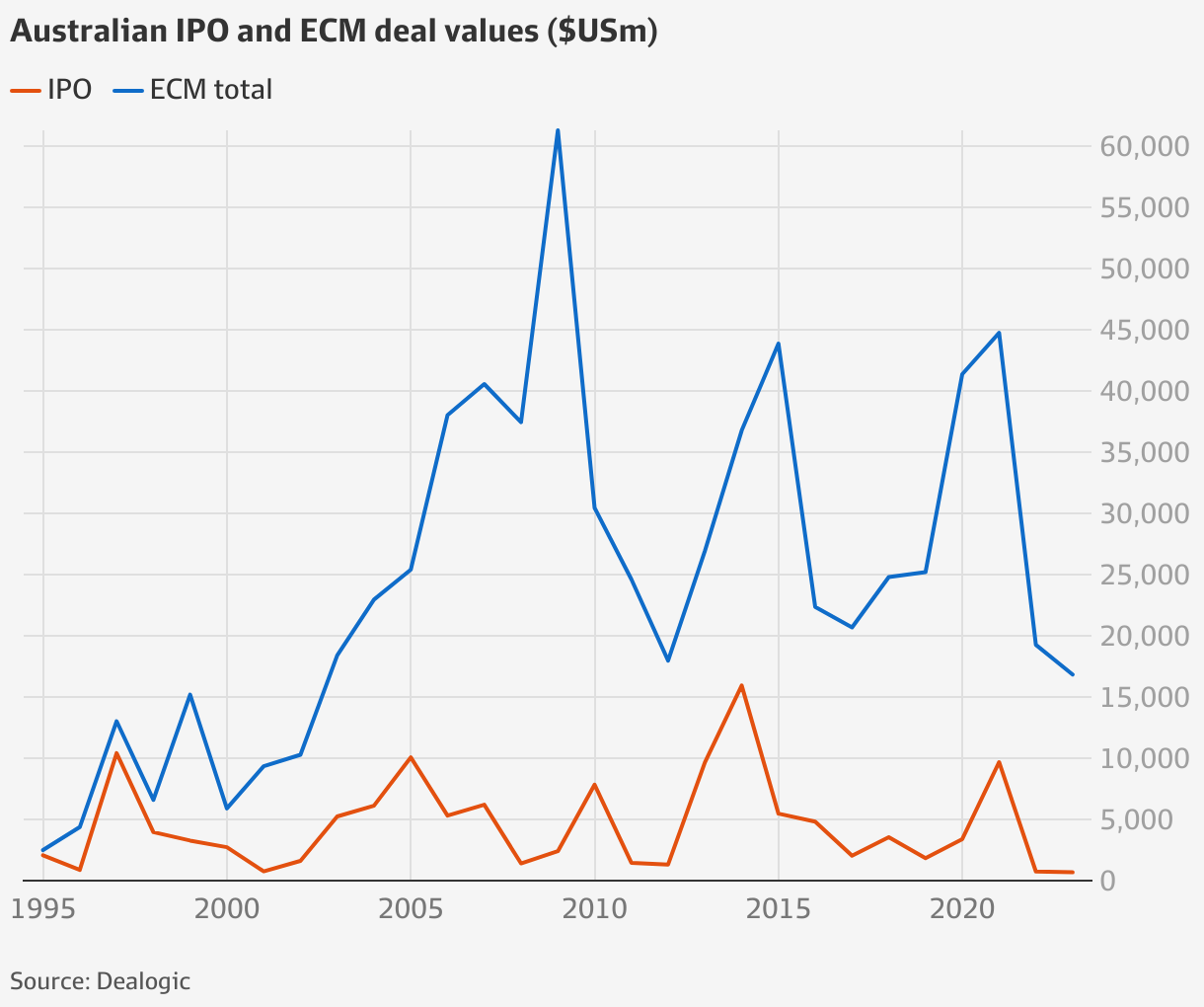

Bankers bet on ASX rally as floats hit 30-year low

“Some really bad surprises have happened, including socioeconomic or political, and the markets have been able to absorb them all,” said Jonas Troeber, JPMorgan’s local co-head of equity capital markets.

Barrenjoey’s Jabe Jerram thinks a billion-dollar IPO raise is possible in 2024.

“Overall [equity capital market] volumes were broadly in line with 2022, markets are up, investor confidence is returning, the conversation has shifted to rates easing, and there hasn’t been a huge wave of collapses.

“It is always difficult to predict if there will be another black swan event, but it looks like the worst is over.”

None of the bankers who spoke to The Australian Financial Review predicted a full-throttle return of IPO roadshows. At best, they are hoping for a few smaller listings between March to June, with larger companies expected to wait until the second half. There are no expectations of a rush of floats.

Charlie Daish, UBS’s head of equity capital markets origination in Australasia, said that in a typical year, IPOs would raise about $6 billion and account for about 14 per cent of total ECM volumes in Australia. For the past two years, this fell to less than 5 per cent, but conditions are improving.

Jonas Troeber, JPMorgan’s ANZ co-head for ECM.

“We’ve obviously had the Q4 rally, and I think it’s too early to call the market open, but there is optimism on interest rates and inflation expectations,” said Mr Daish, whose team ran the Redox float in July. “A number of high-quality candidates have done the work in 2023 for their IPO readiness and will be able to move quickly against the right backdrop which could be towards the late first half.”

Barrenjoey, which ended last year with the top spot on ECM league tables, is similarly hopeful but refraining from predicting a brisk comeback in new listings.

“Whether we see a billion-dollar IPO raise this year is a separate point, but I think the market definitely has capacity for it and certainly can be achieved,” said Jabe Jerram, the investment bank’s ECM co-head.

“At the end of the day, IPOs are a barometer of risk sentiment and whilst the rally to end 2023 is encouraging, a number of those elements – volatility and uncertainty around the macro environment – still persist.”

The turn in investor sentiment that’s held up stockmarkets since September – and helped ASX-listed companies including Treasury Wine Estates, Orora Limited and Karoon Energy secure significant amounts of new financing – is yet to spill into the IPO market.

A key roadblock for recent floats, sustainability of COVID-19 pandemic earnings, is now a thing of past. Most IPO hopefuls will soon have their 2024 financials – or two years of post-pandemic earnings – for fund managers to see, which should help whet fund managers’ appetite.

“We’re not dealing with a situation where it’s a lack of appetite to look at new opportunities or a lack of capital,” said Macquarie Capital’s co-head of ECM Georgina Johnson.

“IPOs are inherently more risky and have a longer lead time. In the current environment investors will be looking for companies and vendors to take a partnering approach across valuation, sell downs, escrows and governance.”

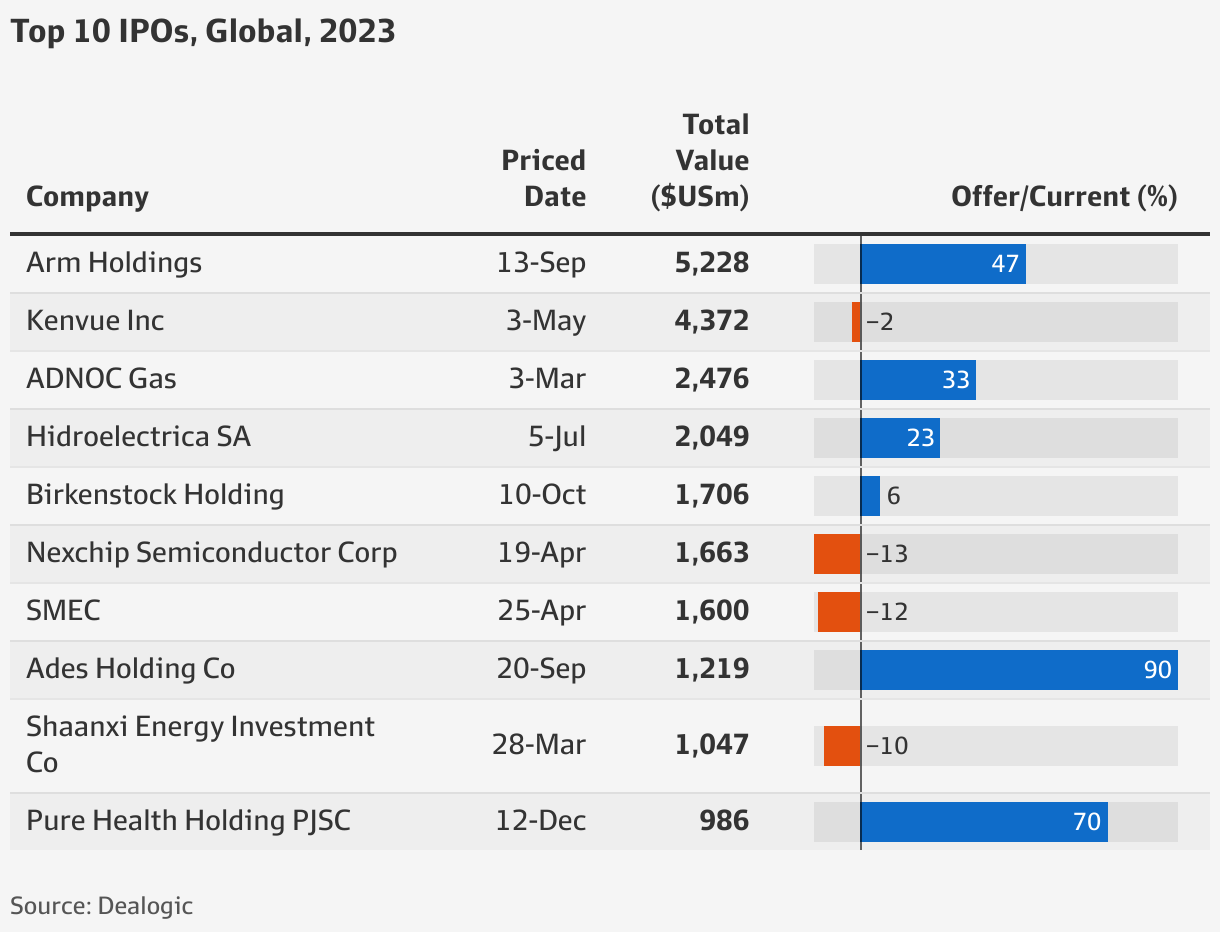

Ms Johnson’s team – alongside Goldman Sachs – is advising data centre business AirTrunk on its options, which are understood to include an IPO, as reported by the Financial Review’s Street Talk column. Should it list, it is expected to be worth $10 billion and would be the biggest IPO since health insurer Medibank Private’s $5.7 billion listing in 2014.

It is now the biggest reported candidate in the IPO pipeline, followed by Bain Capital’s Virgin Australia, grinding media business Molycop, Mexican-themed restaurant chain Guzman y Gomez and freight forwarder Mondiale VGL. On the smaller end, investment platform Mason Stevens has had an advisory lineup ready to go, while Brennan IT, Munro Footwear and Alex Bank have indicated intentions to list or raise capital.

While private equity buyouts could also ensure a healthy supply of float candidates, there are not many businesses in advanced stages of preparing for a listing.

“The big run in IPOs in 2021 somewhat exhausted the pipeline for larger big floats and, if anything, it has been depleted further with the likes of Chemist Warehouse and 7-Eleven pursuing other paths,” said Morgan Stanley’s head of equity capital markets Luke Boeg.

“I think you will see a continued trend of vendors contemplating alternative pathways to an IPO. In particular, we are seeing conversations pick up for pre-IPO capital raises as an intermediary step, where companies are aiming to seed their register with high-quality listed investors that can set it up for an eventual IPO.”

In more ways than one, the ideal IPO candidate of 2024 is no different from the ideal IPO candidate of last year. Bankers say what will reopen the IPO markets is a business with real profits, a real shot at future growth and a management track record. Industrials are expected to have the right of way, with the market still shut for high cash-burn technology businesses.

Georgina Johnson, ECM co-head of ECM for Australia and New Zealand, Macquarie Capital.

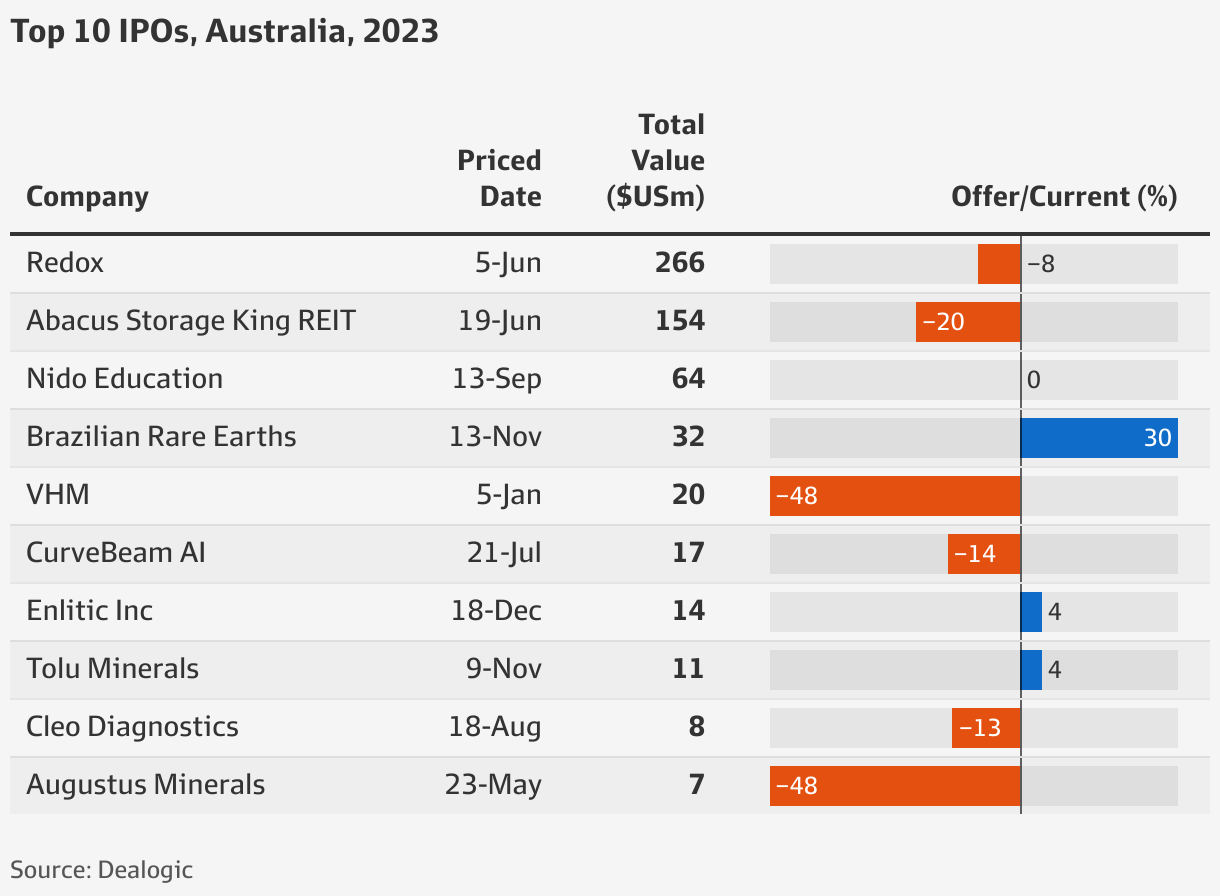

Redox ticked those boxes but has struggled to trade well. And so there’s greater focus than ever on the fine print: how much of the company is floated, at what price, and to whom.

“For the IPO market to truly reopen, we need to see a couple of big floats with decent offer sizes that can properly test the market depth, are appropriately priced and distributed, and trade well in the aftermarket,” said Mr Boeg.

“Marginal IPOs with smaller offer sizes that have no prospect of index inclusion won’t do it. It has to be a must-own for fund managers.”